You should use a debt snowball template if you are planning to pay off your debt. This tool helps you to keep track of the payments you’re making. It can be used to write down all your debts and then decide how much you’ll set aside per month for them. In addition, use a debt reduction calculator to see your debt’s progression.

What is a debt snowball?

The debt snowball technique is a debt reduction plan for those people who owe on more than one account and starting pay off the debt in order of smallest to largest and paying the minimum payments on larger debts. When small debt is paid off then the debtor proceeds to the next larger debt. The debt snowball technique enables you to pay off a debt completely in only a few months. This method will maintain your energy and dedication.

How to use the Debt snowball calculator?

Consider the following steps to use the debt snowball calculator;

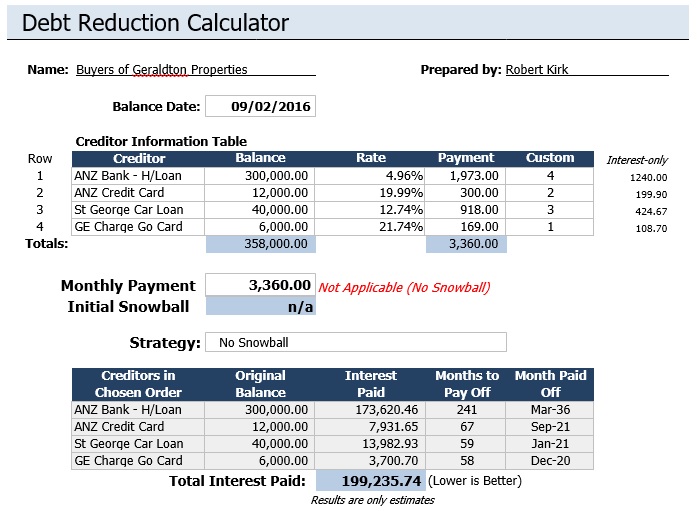

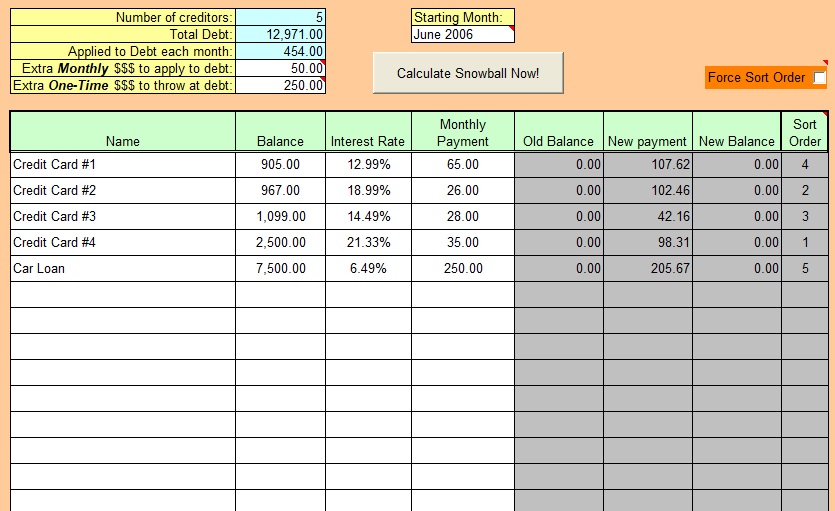

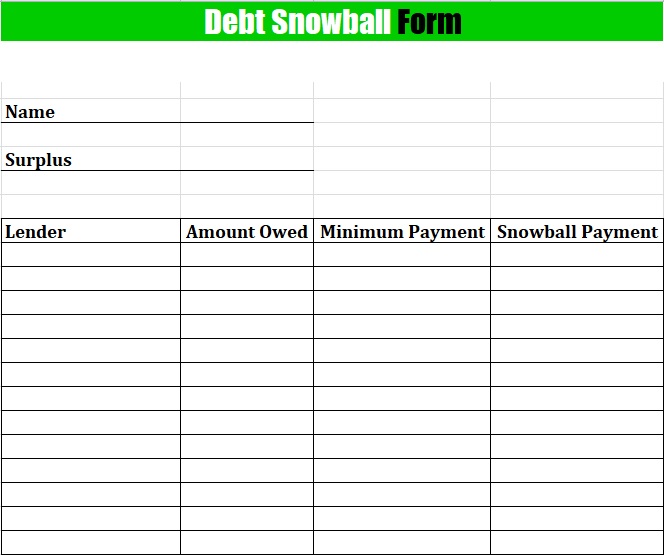

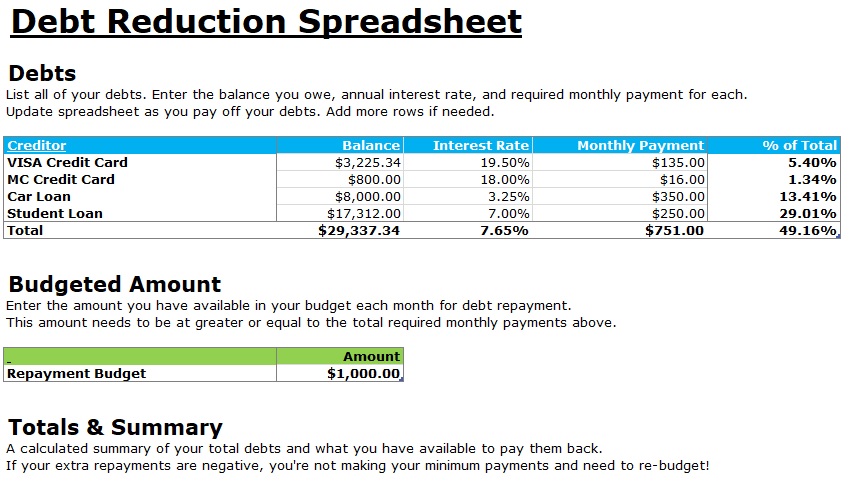

- For all your current debts, write the abbreviated names of the lending institutions, the current balances, and the interest rate information.

- Decide and write the minimum payment that you can pay each month towards your debts. Your initial snowball is the difference between the total minimum payments and your total monthly payment. Keep in mind that at a time this initial snowball is applied to one debt target based on the order defined by your selected strategy.

- In order to see the debts in your selected order, look at the results table.

How does the debt snowball work?

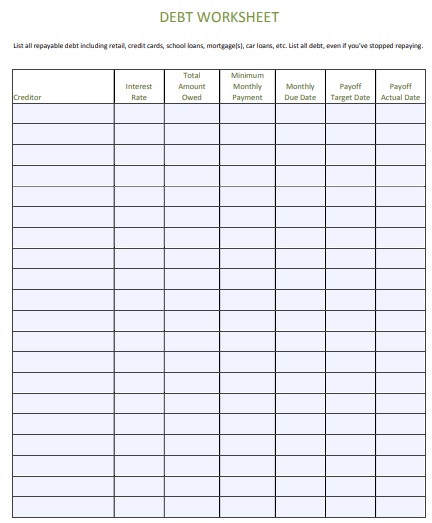

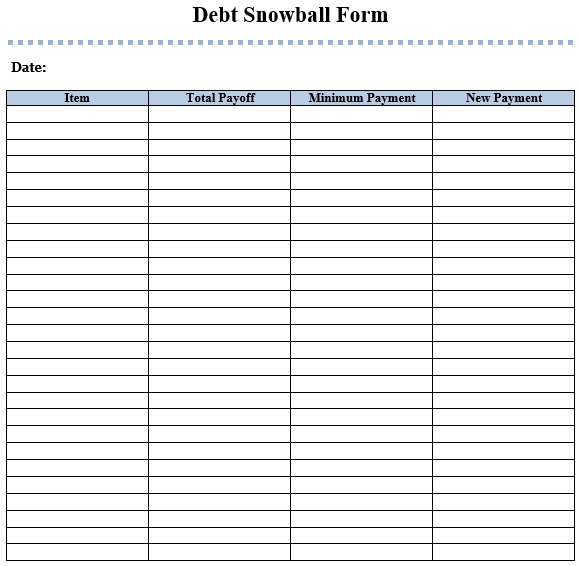

It would be extremely satisfying to know in your heart that you don’t owe any money to anyone. This would mean for most people that they may have extra money every month to spend freely. By using the debt snowball method, you can achieve a debt-free status. You will have to use a debt snowball spreadsheet or a debt snowball form in this method.

Additionally, to keep track of all your debts, you will need a template. Download the sheet so that you can use it for doing calculations and checking your progress. This method is great as it will encourage you early-on. You can take control of your finances by having it and make decision on how much goes into paying off what you owe.

If you want to be debt-free, most people believe that you need to pay off your biggest debts first. But, this isn’t necessarily true as people who do this don’t stay encouraged. In a short amount of time, you won’t be able to cross off your debts. Paying the biggest debt first will take a long time before you can see the fruits of your labor. But, you’ll get the momentum you need from the start with the snowball method.

To pay off all your financial obligations, this debt snowball spreadsheet template method is a way of planning. A debt snowball worksheet and a debt snowball calculator will require in order to do this. Try to use the former to create your plan. Then, you require the latter to come up with the amount and time that you will require to finish your debts. For a lot of people, this method works as the early results inspire them to keep on going.

The debt snowball works in the following way;

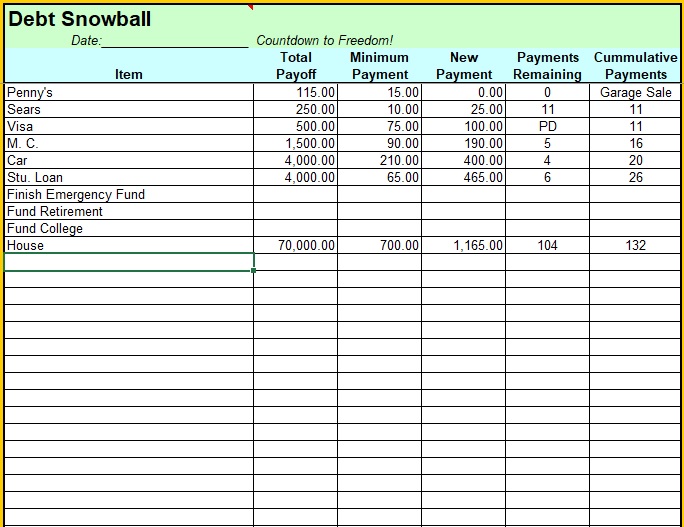

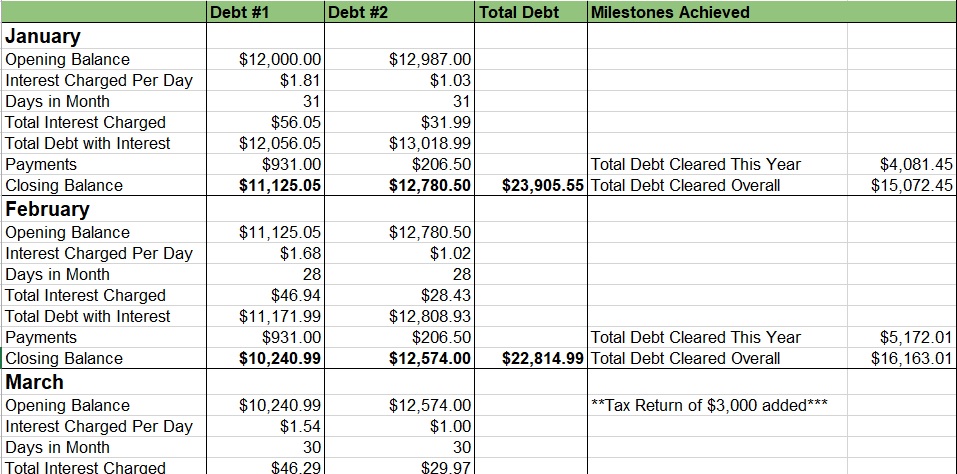

- Firstly, you have to write down all the debts in a column in ascending order i.e. from smallest up to the largest.

- Then, in the next column enter the minimum monthly payment due on every debt.

- Next, pay off the minimum amount on each debt every month.

- After paying the smallest debt then add that amount to whatever the minimum payment that you have paid on the next smallest debt.

- When you have paid off the second debt, repeat the given formula i.e.

Minimum payment due+ amount dedicated to paying off smallest debt = total monthly payment- until all debts have been finished

How do I create a debt snowball spreadsheet?

Here are a few steps that will help you in creating a debt snowball spreadsheet;

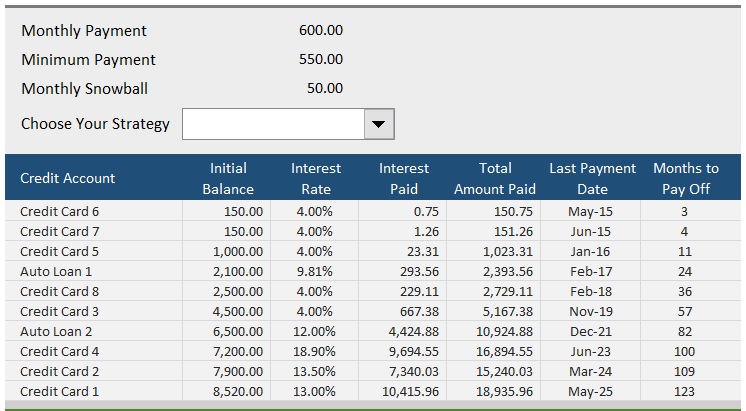

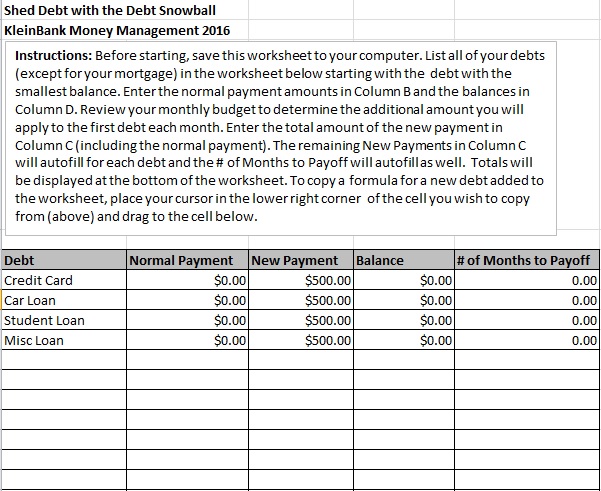

Step#1: Firstly, identify how much money you will pay from your debt every month. By keeping the debt snowball method in your mind, figure out it.

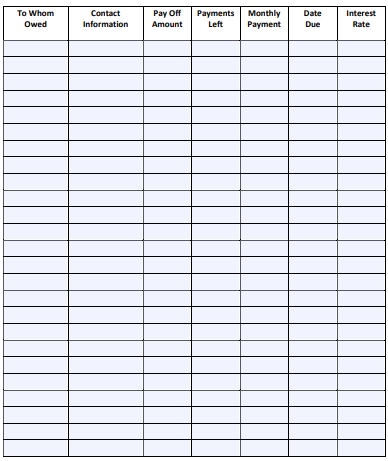

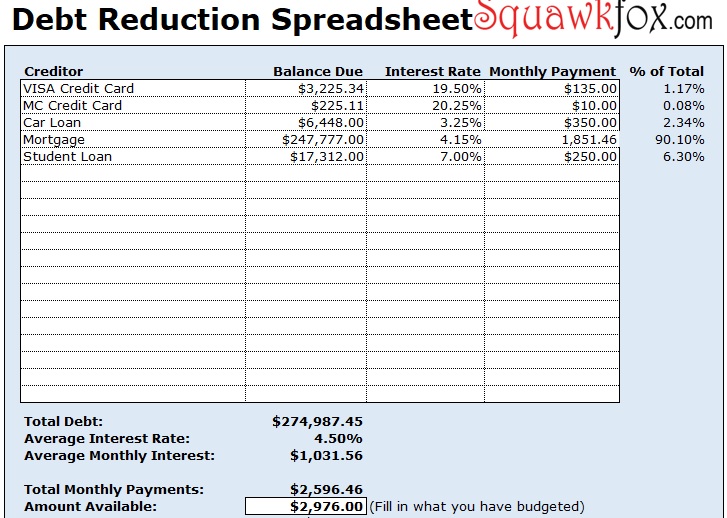

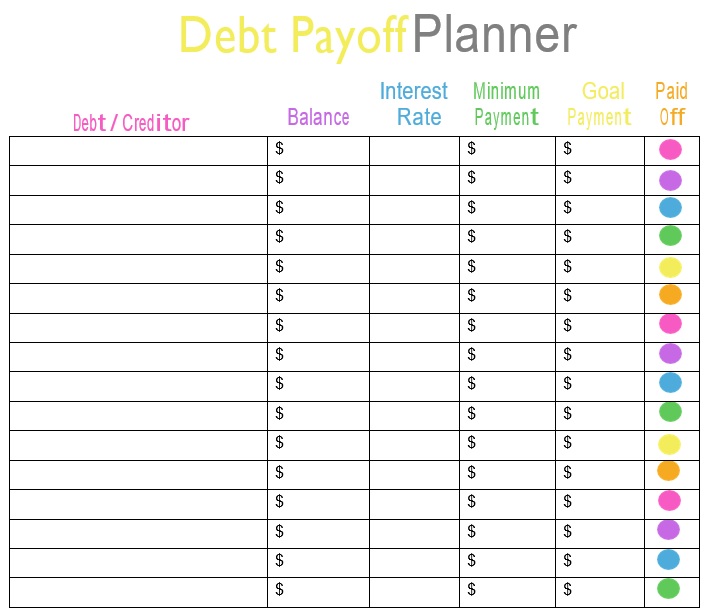

Step#2: Next, open MS Excel to create a spreadsheet. Use six columns i.e.

- Creditor,

- Current balance,

- Interest rate,

- Minimum payment,

- Actual payment,

- And, the payoff date.

However, a spreadsheet is such an easiest way to update your debt list from month to month.

Step#3: The creditors that you plan to pay off enter in the column of ‘Creditors’. Based on the interest rate you can write them from highest to lowest or from lowest to highest balance. If you have a lot of debt to pay off then start with smaller debts it will give you an emotional boost.

Step#4: After that, fill the remaining columns such as current balance, interest rate, minimum payment, and actual payment for every debt. Then, multiply the current balance by the interest rate and sum it together. To get the payoff date to divide the total by the monthly payment.

Step#5: Each month after making a payment update your current balance. When one debt has paid off then update your actual payment for the next debt on the spreadsheet. You have to highlight the paid debt.

How to use your debt snowball spreadsheet to pay off your debts?

To pay off all your debts, you may feel like you’re struggling. Usually, almost everyone in the world feels the same way. You can use various methods and strategies to free yourself of obligations. The debt snowball method stands out among all these methods. You will prioritize small debt payments here.

You will pay attention to pay off the smallest balances. This will give you with faster results. On people’s sense of progress, this method has a more powerful impact. Then, this acts as their encouragement to keep on going until they’ve paid off all of their debts.

You need to make or download a debt snowball form or spreadsheet while using this method. However, many people make this MS Excel.

Consider the following tips for using the spreadsheet;

- Consider the minimum payment that you can place into your debts every month. The faster you can pay off what you owe if the amount is bigger.

- Decide on how much you can dedicate to your smallest debt. You’ll put in more for the smallest one although you’ll be paying a minimum amount to all other debts.

- From the smallest to the largest, list down all your debts. If you know the interest rate then you can also include it each month.

Some other debt-reduction methods:

Variation of the Debt Snowball

Variation of the debt snowball method is for the people who have similar debt balances in their snowball but their interest rates are different. You should organize your debt repayment strategy in descending order so that the higher interest rate is paid off first. This won’t affect your momentum and will save you money.

Stair stepper strategy

This method involves a variation on the debt snowball. It includes the mathematical elements of the debt avalanche. In this method, you have to arrange your debts in the same way as you would for the debt snowball method. Divide your debts into various categories when you are done with that.

Pay off the debts in descending order within those groups. However, you can also start with small debts. But, if you want to keep the momentum of paying off small debts first then start with the highest-interest debt in the small debt group.

User-defined method

The user-defined method is essentially the free-for-all method. It is also referred to as the debt payoff method. When you have owed a family member a personal debt that has been eating you up on the inside then this method can be used. Put this debt at the top of the list. At the bottom of the list, put the debt holder who irritates you and whom you’d rather pay off last. Additionally, this method is ineffective.

The advantages of using a debt snowball method:

Let us discuss below the advantages of using this method to fulfill all your payments;

As time goes by, this method will build momentum

You’ll see results immediately with the debt snowball template method. It would be a lot easier as you’ll focus on your smallest arrears first. You will become able to celebrate the completion of one debt after a short amount of time. From your list early on, you can cross off an obligation with this method. This will encourage you from the start. Unlike, you won’t be able to see the results for some time if you start with the bigger balances.

This way, you may lose interest in paying off what you owe. But, you’ll gradually gain momentum with the snowball method. One at a time, you’ll get to see your debts decreasing.

Negotiating the interest rates

You can use this method on your own. Also, you can use it while paying off debts in financial institutions. You can negotiate the interest rates while making payments to such institutions. By refinancing loans, transferring credit card balances, and more, you can do this. However, you must have a great credit score if you’re planning to do this. If you want to negotiate terms, you should also have a good payment history.

Furthermore, make a call to your credit card company when it comes to paying off credit card debt. You’ll have to request for it if you want to negotiate interest rates. Reference your good payment history in order to enhance your chances of approval. Also, if you’ve been their client for a long time then make a reference to your loyalty to the company. Consider other companies in case your credit card company doesn’t approve your request.

Customize your snowball plan as per your requirements

Don’t write off this method altogether if you can’t negotiate the interest rate. You can also make your own debt repayment plan. You just have to use a debt payoff spreadsheet or a debt snowball worksheet.

Write down all your debts and from the biggest to the smallest, arrange them. After that, by repaying your smallest balance aggressively, start your debt snowball. This will assist you in building your momentum. Then, you can move further to the next one and so on.

Difference between Debt Snowball and Debt Avalanche:

You will organize your debts from the highest to lowest interest rate with the debt avalanche. Thus, it is opposite to the debt snowball method. Depending on the mathematics alone, the debt avalanche method always pays off faster in comparison to the debt snowball method. The debt avalanche method gradually gives you positive reinforcement more.

With the help of the debt snowball method, you will get motivation and you will stay on track. On the other hand, the debt avalanche method may exhaust you during the first few steps. Make an informed choice while deciding between the two because they both work great in their own way.

Does the debt snowball really work?

The debt snowball technique takes a long time and more cost than other debt-relief options such as debt consolidation loans or debt management programs. If you put the right numbers in right place and everything is going on according to momentum then the debt snowball technique also works very well. Hence, this technique is such an encouraging program that can work at paying off debt.